| From | Rep. Andrew Learned <[email protected]> |

| Subject | Out of control prices, Homeowners Insurance Part 4/5: The long game |

| Date | May 19, 2022 6:16 PM |

Links have been removed from this email. Learn more in the FAQ.

Links have been removed from this email. Learn more in the FAQ.

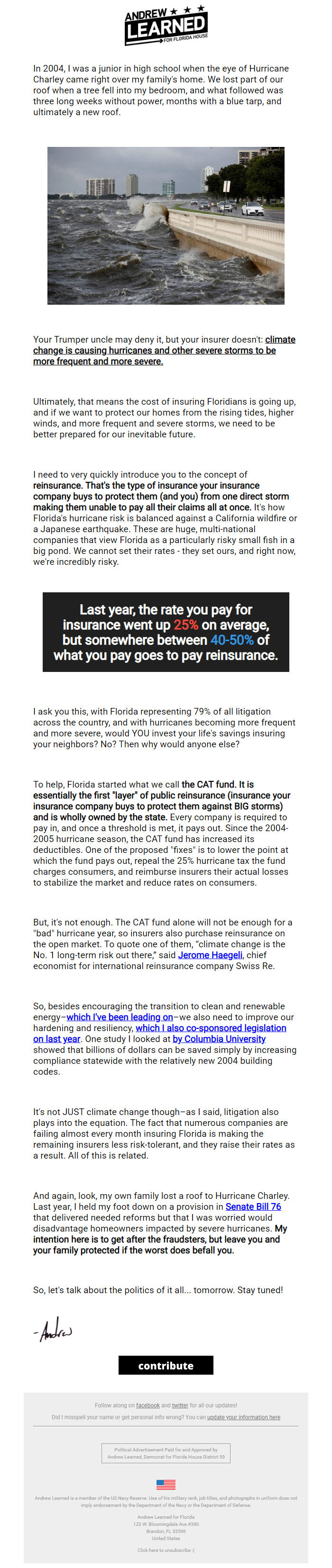

In 2004, I was a junior in high school when the eye of Hurricane Charley came right over my family's home. We lost part of our roof when a tree fell into my bedroom, and what followed was three long weeks without power, months with a blue tarp, and ultimately a new roof.

[[link removed]]

Your Trumper uncle may deny it, but your insurer doesn't: climate change is causing hurricanes and other severe storms to be more frequent and more severe.

Ultimately, that means the cost of insuring Floridians is going up, and if we want to protect our homes from the rising tides, higher winds, and more frequent and severe storms, we need to be better prepared for our inevitable future.

I need to very quickly introduce you to the concept of reinsurance. That's the type of insurance your insurance company buys to protect them (and you) from one direct storm making them unable to pay all their claims all at once. It's how Florida's hurricane risk is balanced against a California wildfire or a Japanese earthquake. These are huge, multi-national companies that view Florida as a particularly risky small fish in a big pond. We cannot set their rates - they set ours, and right now, we're incredibly risky.

Last year, the rate you pay for insurance went up 25% on average, but somewhere between 40-50% of what you pay goes to pay reinsurance.

I ask you this, with Florida representing 79% of all litigation across the country, and with hurricanes becoming more frequent and more severe, would YOU invest your life's savings insuring your neighbors? No? Then why would anyone else?

To help, Florida started what we call the CAT fund. It is essentially the first "layer" of public reinsurance (insurance your insurance company buys to protect them against BIG storms) and is wholly owned by the state. Every company is required to pay in, and once a threshold is met, it pays out. Since the 2004-2005 hurricane season, the CAT fund has increased its deductibles. One of the proposed "fixes" is to lower the point at which the fund pays out, repeal the 25% hurricane tax the fund charges consumers, and reimburse insurers their actual losses to stabilize the market and reduce rates on consumers.

But, it's not enough. The CAT fund alone will not be enough for a "bad" hurricane year, so insurers also purchase reinsurance on the open market. To quote one of them, “climate change is the No. 1 long-term risk out there,” said Jerome Haegeli [[link removed]] , chief economist for international reinsurance company Swiss Re.

So, besides encouraging the transition to clean and renewable energy– which I've been leading on [[link removed]] –we also need to improve our hardening and resiliency, which I also co-sponsored legislation on last year [[link removed]] . One study I looked at by Columbia University [[link removed]] showed that billions of dollars can be saved simply by increasing compliance statewide with the relatively new 2004 building codes.

It's not JUST climate change though–as I said, litigation also plays into the equation. The fact that numerous companies are failing almost every month insuring Florida is making the remaining insurers less risk-tolerant, and they raise their rates as a result. All of this is related.

And again, look, my own family lost a roof to Hurricane Charley. Last year, I held my foot down on a provision in Senate Bill 76 [[link removed]'s%20prohibited%20practices.] that delivered needed reforms but that I was worried would disadvantage homeowners impacted by severe hurricanes. My intention here is to get after the fraudsters, but leave you and your family protected if the worst does befall you.

So, let's talk about the politics of it all... tomorrow. Stay tuned!

Andrew Learned

Candidate for Florida House (FL-69)

AndrewLearned.com

@AndrewLearned on Social: join the conversation!

Political Advertisement Paid for and Approved by Andrew Learned, Democrat for Florida House District 59

Andrew Learned is a member of the US Navy Reserve. Use of his military rank, job titles, and photographs in uniform does not imply endorsement by the Department of the Navy or the Department of Defense.

Andrew Learned for Florida

123 W. Bloomingdale Ave #390

Brandon, FL 33596

United States

Click here to unsubscribe: [link removed] :(

Update your Information Here [[link removed]]

[[link removed]]

Your Trumper uncle may deny it, but your insurer doesn't: climate change is causing hurricanes and other severe storms to be more frequent and more severe.

Ultimately, that means the cost of insuring Floridians is going up, and if we want to protect our homes from the rising tides, higher winds, and more frequent and severe storms, we need to be better prepared for our inevitable future.

I need to very quickly introduce you to the concept of reinsurance. That's the type of insurance your insurance company buys to protect them (and you) from one direct storm making them unable to pay all their claims all at once. It's how Florida's hurricane risk is balanced against a California wildfire or a Japanese earthquake. These are huge, multi-national companies that view Florida as a particularly risky small fish in a big pond. We cannot set their rates - they set ours, and right now, we're incredibly risky.

Last year, the rate you pay for insurance went up 25% on average, but somewhere between 40-50% of what you pay goes to pay reinsurance.

I ask you this, with Florida representing 79% of all litigation across the country, and with hurricanes becoming more frequent and more severe, would YOU invest your life's savings insuring your neighbors? No? Then why would anyone else?

To help, Florida started what we call the CAT fund. It is essentially the first "layer" of public reinsurance (insurance your insurance company buys to protect them against BIG storms) and is wholly owned by the state. Every company is required to pay in, and once a threshold is met, it pays out. Since the 2004-2005 hurricane season, the CAT fund has increased its deductibles. One of the proposed "fixes" is to lower the point at which the fund pays out, repeal the 25% hurricane tax the fund charges consumers, and reimburse insurers their actual losses to stabilize the market and reduce rates on consumers.

But, it's not enough. The CAT fund alone will not be enough for a "bad" hurricane year, so insurers also purchase reinsurance on the open market. To quote one of them, “climate change is the No. 1 long-term risk out there,” said Jerome Haegeli [[link removed]] , chief economist for international reinsurance company Swiss Re.

So, besides encouraging the transition to clean and renewable energy– which I've been leading on [[link removed]] –we also need to improve our hardening and resiliency, which I also co-sponsored legislation on last year [[link removed]] . One study I looked at by Columbia University [[link removed]] showed that billions of dollars can be saved simply by increasing compliance statewide with the relatively new 2004 building codes.

It's not JUST climate change though–as I said, litigation also plays into the equation. The fact that numerous companies are failing almost every month insuring Florida is making the remaining insurers less risk-tolerant, and they raise their rates as a result. All of this is related.

And again, look, my own family lost a roof to Hurricane Charley. Last year, I held my foot down on a provision in Senate Bill 76 [[link removed]'s%20prohibited%20practices.] that delivered needed reforms but that I was worried would disadvantage homeowners impacted by severe hurricanes. My intention here is to get after the fraudsters, but leave you and your family protected if the worst does befall you.

So, let's talk about the politics of it all... tomorrow. Stay tuned!

Andrew Learned

Candidate for Florida House (FL-69)

AndrewLearned.com

@AndrewLearned on Social: join the conversation!

Political Advertisement Paid for and Approved by Andrew Learned, Democrat for Florida House District 59

Andrew Learned is a member of the US Navy Reserve. Use of his military rank, job titles, and photographs in uniform does not imply endorsement by the Department of the Navy or the Department of Defense.

Andrew Learned for Florida

123 W. Bloomingdale Ave #390

Brandon, FL 33596

United States

Click here to unsubscribe: [link removed] :(

Update your Information Here [[link removed]]

Message Analysis

- Sender: Andrew Learned

- Political Party: Democratic

- Country: United States

- State/Locality: Florida

- Office: United States House of Representatives