| From | Badger Institute <[email protected]> |

| Subject | Wisconsin Legislature Passes Several Pro-Growth Tax Reforms |

| Date | July 1, 2021 8:00 PM |

Links have been removed from this email. Learn more in the FAQ.

Links have been removed from this email. Learn more in the FAQ.

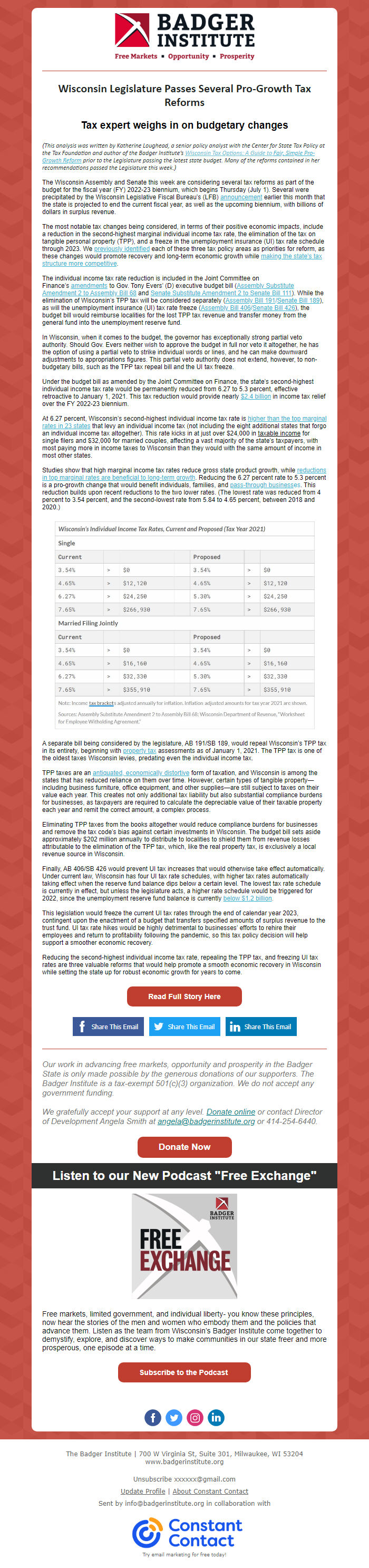

Tax expert weighs in on budgetary changes. Wisconsin Legislature Passes Several Pro-Growth Tax Reforms Tax expert weighs in on budgetary changes (This analysis was written by Katherine Loughead, a senior policy analyst with the Center for State Tax Policy at the Tax Foundation and author of the Badger Institute’s Wisconsin Tax Options: A Guide to Fair, Simple Pro-Growth Reform prior to the Legislature passing the latest state budget. Many of the reforms contained in her recommendations passed the Legislature this week.) The Wisconsin Assembly and Senate this week are considering several tax reforms as part of the budget for the fiscal year (FY) 2022-23 biennium, which begins Thursday (July 1). Several were precipitated by the Wisconsin Legislative Fiscal Bureau’s (LFB) announcement earlier this month that the state is projected to end the current fiscal year, as well as the upcoming biennium, with billions of dollars in surplus revenue. The most notable tax changes being considered, in terms of their positive economic impacts, include a reduction in the second-highest marginal individual income tax rate, the elimination of the tax on tangible personal property (TPP), and a freeze in the unemployment insurance (UI) tax rate schedule through 2023. We previously identified each of these three tax policy areas as priorities for reform, as these changes would promote recovery and long-term economic growth while making the state’s tax structure more competitive. The individual income tax rate reduction is included in the Joint Committee on Finance’s amendments to Gov. Tony Evers’ (D) executive budget bill (Assembly Substitute Amendment 2 to Assembly Bill 68 and Senate Substitute Amendment 2 to Senate Bill 111). While the elimination of Wisconsin’s TPP tax will be considered separately (Assembly Bill 191/Senate Bill 189), as will the unemployment insurance (UI) tax rate freeze (Assembly Bill 406/Senate Bill 426), the budget bill would reimburse localities for the lost TPP tax revenue and transfer money from the general fund into the unemployment reserve fund. In Wisconsin, when it comes to the budget, the governor has exceptionally strong partial veto authority. Should Gov. Evers neither wish to approve the budget in full nor veto it altogether, he has the option of using a partial veto to strike individual words or lines, and he can make downward adjustments to appropriations figures. This partial veto authority does not extend, however, to non-budgetary bills, such as the TPP tax repeal bill and the UI tax freeze. Under the budget bill as amended by the Joint Committee on Finance, the state’s second-highest individual income tax rate would be permanently reduced from 6.27 to 5.3 percent, effective retroactive to January 1, 2021. This tax reduction would provide nearly $2.4 billion in income tax relief over the FY 2022-23 biennium. At 6.27 percent, Wisconsin’s second-highest individual income tax rate is higher than the top marginal rates in 23 states that levy an individual income tax (not including the eight additional states that forgo an individual income tax altogether). This rate kicks in at just over $24,000 in taxable income for single filers and $32,000 for married couples, affecting a vast majority of the state’s taxpayers, with most paying more in income taxes to Wisconsin than they would with the same amount of income in most other states. Studies show that high marginal income tax rates reduce gross state product growth, while reductions in top marginal rates are beneficial to long-term growth. Reducing the 6.27 percent rate to 5.3 percent is a pro-growth change that would benefit individuals, families, and pass-through businesses. This reduction builds upon recent reductions to the two lower rates. (The lowest rate was reduced from 4 percent to 3.54 percent, and the second-lowest rate from 5.84 to 4.65 percent, between 2018 and 2020.) A separate bill being considered by the legislature, AB 191/SB 189, would repeal Wisconsin’s TPP tax in its entirety, beginning with property tax assessments as of January 1, 2021. The TPP tax is one of the oldest taxes Wisconsin levies, predating even the individual income tax. TPP taxes are an antiquated, economically distortive form of taxation, and Wisconsin is among the states that has reduced reliance on them over time. However, certain types of tangible property— including business furniture, office equipment, and other supplies—are still subject to taxes on their value each year. This creates not only additional tax liability but also substantial compliance burdens for businesses, as taxpayers are required to calculate the depreciable value of their taxable property each year and remit the correct amount, a complex process. Eliminating TPP taxes from the books altogether would reduce compliance burdens for businesses and remove the tax code’s bias against certain investments in Wisconsin. The budget bill sets aside approximately $202 million annually to distribute to localities to shield them from revenue losses attributable to the elimination of the TPP tax, which, like the real property tax, is exclusively a local revenue source in Wisconsin. Finally, AB 406/SB 426 would prevent UI tax increases that would otherwise take effect automatically. Under current law, Wisconsin has four UI tax rate schedules, with higher tax rates automatically taking effect when the reserve fund balance dips below a certain level. The lowest tax rate schedule is currently in effect, but unless the legislature acts, a higher rate schedule would be triggered for 2022, since the unemployment reserve fund balance is currently below $1.2 billion. This legislation would freeze the current UI tax rates through the end of calendar year 2023, contingent upon the enactment of a budget that transfers specified amounts of surplus revenue to the trust fund. UI tax rate hikes would be highly detrimental to businesses’ efforts to rehire their employees and return to profitability following the pandemic, so this tax policy decision will help support a smoother economic recovery. Reducing the second-highest individual income tax rate, repealing the TPP tax, and freezing UI tax rates are three valuable reforms that would help promote a smooth economic recovery in Wisconsin while setting the state up for robust economic growth for years to come. Read Full Story Here Share This Email Share This Email Share This Email Our work in advancing free markets, opportunity and prosperity in the Badger State is only made possible by the generous donations of our supporters. The Badger Institute is a tax-exempt 501(c)(3) organization. We do not accept any government funding. We gratefully accept your support at any level. Donate online or contact Director of Development Angela Smith at [email protected] or 414-254-6440. Donate Now Listen to our New Podcast "Free Exchange" Free markets, limited government, and individual liberty- you know these principles, now hear the stories of the men and women who embody them and the policies that advance them. Listen as the team from Wisconsin’s Badger Institute come together to demystify, explore, and discover ways to make communities in our state freer and more prosperous, one episode at a time. Subscribe to the Podcast The Badger Institute | 700 W Virginia St, Suite 301, Milwaukee, WI 53204 www.badgerinstitute.org Unsubscribe [email protected] Update Profile | About Constant Contact Sent by [email protected] in collaboration with Try email marketing for free today!

Message Analysis

- Sender: Badger Institute

- Political Party: n/a

- Country: United States

- State/Locality: Wisconsin

- Office: n/a

-

Email Providers:

- Constant Contact