Editor's Note: Marc Chaikin, the 60-year Wall Street legend who called Nvidia before it soared 45,000%, just came forward with another huge opportunity he's spotted in the AI space. While the media is caught up in "SpaceX fever" right now, the under-the-radar event Marc reveals below could give you access to three brand-new AI IPOs in a rare deal known as a "starburst." You may never get a chance to take part in one of these again in your life... and while it's speculative, Marc urges readers to get in before July 22nd while everyone's attention is elsewhere...

Dear Reader,

A tech firm that's been called "the unseen winner of the AI race" could soon break itself up into three separate companies.

The next Netflix...

The next Tesla...

And the next Amazon are all poised to spin off just from this one stock.

That would create a once-in-a-lifetime opportunity for investors who buy shares in the company before it happens.

Buy shares of this stock before July 22nd, and you could get the same amount of free shares automatically deposited in your account for each spinoff.

Meaning, 10 shares could turn into 30 shares overnight.

And you could wake up with the world's newest, hottest tech disruptors all sitting in your account – with no extra work on your part.

Believe me, when it happens, it feels like magic, but it's actually something called a "starburst."

This brilliant type of spinoff is especially rare in the tech industry.

And if the starburst announcement goes public (and it hasn't yet), it's going to be all the media talks about for a while afterward.

This potential "starburst" is my No. 1 recommendation for how average folks can set themselves up to benefit from what I'm calling AI's "jump to lightspeed" moment.

Sincerely,

Marc Chaikin

Founder, Chaikin Analytics

P.S. In 2021, GE announced a starburst when the stock traded at just $67 per share. They rolled out the deal in stages, and when it was done, shareholders owned three companies instead of just one. The share prices on those once they were individually valued? $75... $300... $614... That means that one starburst unlocked $184 billion for investors. I predict this potential AI starburst will be orders of magnitude larger. And I believe this stock could see a major jump in share price on July 22nd. Get the details when you click here...

3 Biotech Firms With Major Potential Catalysts in the Coming Months

Reported by Nathan Reiff. Originally Published: 6/21/2026.

Key Points

- For biopharma companies, a huge amount relies on key FDA approvals or strong data readouts from clinical trials.

- Two companies with promising drug candidates in line for potential upcoming approvals are VERA and KRYS.

- ADMA may be in a different position thanks to its strong preexisting products but still has a potential catalyst on the horizon.

- Special Report: The company SpaceX cannot operate without

As Big Pharma braces for a looming patent cliff that threatens billions in revenue, a different group of companies is chasing the opposite story: a single breakthrough that could define their future. For these smaller players, one strong trial readout or FDA approval can mean the difference between a breakout and a bust.

Below, we look at several companies that investors willing to take on a bit more risk in the pharma industry may want to keep an eye on. Two have key FDA decisions on the horizon, though on slightly different timelines. The third takes a different approach: as a company with multiple products already on the market, it doesn't rely as heavily on a single strong data release or FDA announcement, though it can still benefit from those developments.

Vera Makes Big Moves in the Nephrology Space

ALERT: Drop these 5 stocks before the market opens tomorrow! (Ad)

The Wall Street Journal is already raising the alarm about a potential market crash, and Weiss Ratings research points to the first half of 2026 as a particularly rough stretch for certain holdings.

Some of America's most popular stocks could take serious damage as a radical market shift plays out. Analysts at Weiss Ratings have identified five names you may want to remove from your portfolio before this unfolds.

If any of these are in your portfolio, now is the time to review your positions.

See the 5 stocks to avoidA clinical-stage biotech company developing immunotherapies for autoimmune and inflammatory diseases, Vera Therapeutics (NASDAQ: VERA) has a major pending FDA decision that could be instrumental for the company. Vera is working toward a Biologics License Application (BLA) for atacicept, an investigational drug with the potential to address IgA nephropathy, an autoimmune kidney disease.

In early June, the company reported an encouraging update, including alignment with the FDA on a revised ORIGIN 3 eGFR analysis plan and an accelerated timeline. If this goes well in Q3, Vera will likely submit its BLA before the end of the year.

If atacicept receives full approval, it could unlock major commercial potential in the fast-growing $20 billion global nephrology market. On the other hand, a negative decision or even a delay in the eGFR process could be detrimental to VERA shares.

For now, analysts remain bullish: 10 out of 12 ratings are Buys, and Wall Street expects the stock to climb by 120%.

A Gene Therapy Winner Awaits 2 New Sets of Data

Krystal Biotech (NASDAQ: KRYS) is a gene therapy company developing novel treatments for dermatological diseases. The company has already achieved notable success with Vyjuvek, the first gene therapy ever approved for a skin condition. That may give investors additional confidence as the company prepares for two upcoming data readouts that could add even more momentum. Vyjuvek revenue was $116 million in the first quarter, up 32% year over year (YOY).

The firm's KB803 is currently in trials evaluating its potential as a treatment for corneal abrasion in patients with dystrophic epidermolysis bullosa, with top-line results expected by the end of this year. Additionally, Krystal has a second candidate in line for a registrational data readout in 2026: KB801 is being studied as a potential treatment for neurotrophic keratitis.

Though niche, each of these drugs could address previously underserved corners of the market and strengthen Krystal's overall portfolio significantly.

Ten out of 12 analysts call KRYS shares a Buy, although with more than 40% returns year to date (YTD), investors may be wondering how much upside remains in the near term.

An Established Player With a Promising Long-Horizon Prospect

ADMA Biologics (NASDAQ: ADMA) is a biopharma company that develops plasma-based biologics to treat immunodeficiency and infectious diseases. The company is in a different position from others in the field because it already has multiple products on the market and strong revenue, including 28% YOY growth last quarter from ASCENIV.

As such, ADMA is less reliant on promising news from the FDA or clinical trial readouts, although those updates can still catalyze additional growth. Instead, part of ADMA's appeal comes from its margin expansion, which has been helped by a new set of manufacturing efficiencies implemented over the last several quarters.

That is not to say the company has no products on the horizon, though, and SG-001—an investigative hyperimmune globulin candidate for pneumococcal disease—is among the most promising.

Investors might expect a boost to ADMA stock if and when positive results are released for this candidate, but in the meantime, the attraction may be more focused on the stability that ADMA's existing products already provide.

ADMA shares are down considerably YTD, falling by more than 50% over that period. However, that makes the company's value proposition more attractive, particularly as its price-to-earnings (P/E) ratio of 12 is well below the broader sector. Plus, analysts still see plenty of room for growth based on upside forecasts of more than 130%.

Copa Holdings May Be the Airline Stock Built to Break Out

Reported by Thomas Hughes. Originally Published: 6/23/2026.

Key Points

- Copa Holdings has a lot going for it, making it a win for investors seeking growth and capital returns.

- A hub-and-spoke setup enables highly efficient airline operations.

- Analysts are forecasting this emerging market stock to reach new highs in 2026.

- Special Report: The company SpaceX cannot operate without

Copa Holdings (NYSE: CPA) is an airline stock with structural advantages, a strong market position, and capital returns that make it an almost ideal investment. Its strength as a leading Latin American carrier provides emerging-market exposure through a critical infrastructure and services story. Its key advantage is a hub-and-spoke network centered on The Hub of the Americas. This is the company’s headquarters at Tocumen International Airport, a centralized location that enables highly efficient operations across the system.

The setup supports the region's leading service record and the No. 2 record globally, with an average on-time rate of about 90% and completion rates trending in the 99% range. In addition to the hub-and-spoke model, Tocumen’s central location makes connections quick and efficient, further enhanced by terminal placement. Passengers don’t have to worry about customs or transit when transitioning from one flight to the next. In addition, the company operates a single-type fleet, which further controls costs by limiting maintenance hassles, training needs, and parts inventory.

Copa Holdings Accelerates Growth in Q1 2026

ALERT: Drop these 5 stocks before the market opens tomorrow! (Ad)

The Wall Street Journal is already raising the alarm about a potential market crash, and Weiss Ratings research points to the first half of 2026 as a particularly rough stretch for certain holdings.

Some of America's most popular stocks could take serious damage as a radical market shift plays out. Analysts at Weiss Ratings have identified five names you may want to remove from your portfolio before this unfolds.

If any of these are in your portfolio, now is the time to review your positions.

See the 5 stocks to avoidCopa Holdings had a strong Q1, with revenue growing 17% to just over $1 billion, underscoring the company's strength. The top line exceeded MarketBeat’s consensus estimate by a wide margin, accelerating from the prior quarter and year on increased capacity and demand. A bullish detail is that passenger traffic increased 15% on a 14% increase in capacity, helping drive margin strength, further supported by improved revenue per mile.

Margin performance was also strong. The company widened both operating and net margins despite higher costs, particularly fuel. GAAP earnings grew at an accelerated 20.5% pace, exceeding the consensus estimate by 73 cents, or nearly 1,650 basis points (bps). Looking ahead, the company issued a cautious Q2 forecast, citing fuel cost headwinds, but remained positive for the year and is forecasting 17% revenue growth.

Bullish Cash Flow and Capital Return Outlook Drive CPA Price Action

Copa Holdings' highly efficient business generates healthy cash flow and supports capital returns, including dividends and share buybacks. Dividends are approximately 40% of earnings and appear sustainable in 2026, yielding approximately 4.5% with shares trading near historically high levels.

Distribution increases are expected given the revenue and growth outlook, and they will likely continue at a robust, double-digit pace in the coming years. Share buybacks are less aggressive but still add value, reducing the share count by an average of 0.3% over the trailing 12 months (TTM).

Institutional activity is mixed, with the balance bullish but relatively flat on a trailing 12-month basis as of mid-year. However, institutions provide solid support, owning about 70% of the shares, and analysts are increasingly bullish.

MarketBeat data shows increasing coverage, improving sentiment, and rising price targets, with a consensus Buy rating and a forecast for fresh all-time highs. Short interest does not appear to be an issue. It is slightly elevated at around 4% but not alarming, and is more likely tied to hedging activity than outright bearish positioning.

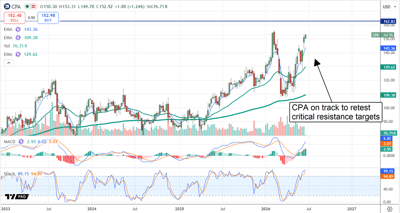

Copa Holdings Advances: Approaches Critical Threshold

Copa Holdings’ price action remains bullish in Q2. The stock is advancing and on track to test resistance at its current all-time high. Bullish signals in the MACD and stochastic suggest the retest could come soon, potentially by year’s end, and new highs are possible. Setting new highs would be significant, as they would be the first fresh highs in over a decade and could open the door to a much larger move.

In this scenario, the base case is worth the dollar value of the existing trading range, which runs from $120. A move to $280 is possible if a fresh high is set. If not, CPA shares may remain range-bound indefinitely, but that is not expected given the growth and capital return outlook.

Copa Holdings' business is supported by robust demand in a major emerging market region. Latin America is a leading growth pillar internationally, driven by industrialization and middle-class expansion, which are fueling demand for business and leisure travel. Consistent capital returns are expected over time. The biggest risk for Copa is geopolitical. Not only can conflicts outside the region impair travel demand, but internal issues could disrupt business. Numerous international agreements help enable easy, free-flowing traffic among many of the nations served.

Copa Holdings’ balance sheet is not among its risks. The company maintains low leverage and ample cash, which equaled 40% of TTM revenue at the end of Q1. The likely outcome is that Copa Holdings will continue to execute its strategy, investing in growth while returning capital to investors.

This email content is a sponsored message sent on behalf of Chaikin Analytics, a third-party advertiser of MarketBeat. Why did I receive this message?.

This ad is sent on behalf of Chaikin Analytics, 201 King Of Prussia Rd., Suite 650, Radnor, PA 19087. If you would like to optout from receiving offers from Chaikin Analytics please click here.

If you have questions or concerns about your account, please feel free to email MarketBeat's South Dakota based support team at [email protected].

If you would no longer like to receive promotional emails from MarketBeat advertisers, you can unsubscribe or manage your mailing preferences here.

© 2006-2026 MarketBeat Media, LLC.

345 N Reid Place #620, Sioux Falls, SD 57103. USA..