D-Wave's long-awaited Q1 2026 earnings appear rough on the surface, with plunging revenue and widening losses, but many bright spots are... ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ |

| | Written by Nathan Reiff

Earnings season is a pivotal moment for many stocks, but particularly for firms in a fledgling industry like quantum computing. When major player IonQ Inc. (NYSE: IONQ) reported results for the first quarter of 2026 in early May, investors took note of promising revenue growth, a raise to full-year guidance relative to prior projections, and a strong showing in both partnerships and system sales. Still, a crucial piece of the puzzle—profitability—remains missing.

Now, other big names in the pure-play quantum sphere are sharing their own results, including from firms like D-Wave Quantum Inc. (NYSE: QBTS) and Rigetti Computing (NASDAQ: RGTI). D-Wave, known for its sizable cash holdings and recent purchase of Quantum Circuits Inc., stands out for its dual focus on two distinct technological approaches to quantum computing.

Like IonQ, the company noted several compelling developments in its Q1 2026 earnings, particularly in bookings, sales pipeline, and technological advances.

However, top- and bottom-line performance may have contributed to a post-earnings selloff that brought the share price down 7% on May 12, reversing the recent mini-rally initiated in April.

The Bright Spots in D-Wave's Earnings: Bookings, Recurring Revenue, Sales Pipeline, and MoreA number of highlights emerge from a closer look at D-Wave's first quarter of the new year. Notably, quarterly bookings reached $33.4 million, a record for Q1 and a massive increase of about 2,000% year-over-year (YOY). This figure is impressive on its own, but one of the real strengths here is D-Wave's major growth to its quantum-computing-as-a-service (QCaaS) business, which climbed by 15% YOY to $1.8 million in revenue. QCaaS positions D-Wave to be able to build recurring revenue into its stream, which could be crucial in its efforts to achieve sustainable profitability. A $10-million enterprise QCaaS agreement from Q1 was a major driving factor here.

The company's sales pipeline is shining as well, with growth of more than 100% sequentially to Q1 2026. D-Wave sees system sales—the lion's share of its revenue so far—totaling two or three per year going forward, with at least two projected for 2026. These big-ticket sales do not necessarily mean recurring revenue, but they vastly outsize other revenue streams for the firm at this point.

Technological advances are also crucial for any quantum computing company, and D-Wave highlighted some important ones for the first three months of the year. A standout achievement for the company is its roadmap to 100 logical qubits, a major technological breakthrough, which it believes can be achieved by 2032.

Finally, investors have been waiting for signs as to whether D-Wave has been able to maintain its historically strong cash position. With more than $588 million in cash and equivalents as of the end of the quarter, the company's reserves remain healthy.

The Reason for the Share Price DeclineIt's difficult for D-Wave to avoid negative headlines for its top- and bottom-line performance in the quarter, despite all of the successes above. Notably, revenue of $2.9 million was down more than 80% YOY and came in about $1.3 million below analyst predictions. Though losses per share beat predictions by 3 cents, they nonetheless widened by 3 cents relative to the prior-year quarter.

A closer look may give long-term D-Wave investors some comfort. Part of the reason for the seemingly-massive revenue slippage is the fact that Q1 of last year saw the sale of a quantum annealing computer system for nearly $13 million. A single transaction can have a major impact on revenue performance, particularly when overall revenue is so low.

Still, that D-Wave is so susceptible to these significant shifts based on the timing of an individual system sale is a reflection of how reliant the company has been on these types of one-off deals. Investors will surely be happy to see the company move toward a more predictable, consistent revenue stream.

Investors in the quantum computing space will need to evaluate whether D-Wave is still a suitable target based on its performance relative to its peers (for one thing, Rigetti announced on the same day that its Q1 2026 revenue roughly tripled YOY to $4.4 million).

The path toward profitability may have become somewhat clearer based on QCaaS performance, but widening losses and the sizable gap between expected revenue and actual performance suggest that there may still be significant ground to cover.

D-Wave shares remain a Moderate Buy, with 14 out of 17 analysts bullish on the stock.

Read This Story Online Read This Story Online |  A little-known stock pick with money-doubling potential over the next year is revealed for free in the first three minutes of a new video. This company is a critical piece of Elon Musk's fast-growing Starlink technology. It could climb 100 percent or more over the next year as Elon brings Starlink public in what may be the biggest IPO in history. No credit card is required to get the ticker. Watch the free video to get the ticker today. |

| Written by Thomas Hughes

Nebius Group (NASDAQ: NBIS) is another example of a company in an AI-driven feedback loop. The rapid rise of AI infrastructure enables AI model training, which in turn enables inference, outcomes, use cases and increased demand.

Because outcomes tend to be positive, the technology advances with each cycle, strengthening the trend in a potentially indefinite loop. Nebius is well-positioned to benefit, as it provides both the infrastructure for training and inference and tools to support its development.

Nebius' position was reflected in its recent earnings results, released May 13. The company continues to invest, and, according to CEO Arkady Volozh, unprecedented demand exceeds capacity. This suggests that upcoming results will further sustain the trend of outperformance relative to market expectations, and strength will continue until sufficient capacity is built. Based on the demand trends seen across the AI stack, including GPUs, CPUs, memory, and nuts-and-bolts plays in connectivity and networking, that won’t happen for at least a few years.

Nebius Debt Is a Concern, Offset by Rapidly Expanding LeverageNebius' growing debt is a concern, as it blossomed during Q1, but less so than it was just a quarter ago. The offsetting details include quarterly results showing top- and bottom-line outperformance in Q1 and highly visible evidence that the company can profit at scale. Revenue surged by nearly 700%, outpacing the consensus estimate by several hundred basis points, underpinned by hyperscaler demand.

The impact on margin was significant, with leverage evident across all metrics. Gross margin improved by 2,300 basis points (bps), compounded by high-double-digit declines in R&D, G&A, and expenses margins, which left the company’s bottom line in much better shape than expected. The critical detail is that non-GAAP earnings per share of negative 23 cents outpaced the consensus by 58 cents, offering the market a pleasant surprise.

As concerning as Nebius' rapid increase in debt may be, it is offset by balance sheet strength, cash flow, and a robust business pipeline. Balance sheet highlights include cash more than doubling, current and total assets rising, and equity increasing despite the increased debt. Debt leverage is also low, at less than 1X, given the more than $9 billion in cash, with the company’s core business experiencing robust demand. The likely outcome is that Nebius will have little trouble servicing its load and paying it off over time.

Nebius can be expected to continue investing, as it plans to deploy up to $20 billion in AI-related capital expenditure (CapEx) this year alone, but its pipeline more than offsets the strength. Deals in Q1 increased the backlog by approximately 250% to 4GW of contracted capacity, underpinned by hyperscalers such as Meta Platforms (NASDAQ: META), which is sufficient to more than double the company’s current-year revenue outlook. Plans now include a new AI factory in Pennsylvania, adding up to 1.2GW of capacity to the rapidly expanding network.

Analysts in Catch-Up Mode, Underpinning NBIS Stock Price ActionThe analyst trends are bullish for NBIS, and the company continues to fire on all cylinders, forcing them to respond. As it stands, the trends include increasing coverage, firming sentiment, a 73% Buy-side bias to the Moderate Buy rating, and an uptrend in the consensus price target.

The only bad news is that price action is outpacing the consensus, setting the stage for a potential price correction. However, given the current trends, price corrections are likely to be buying opportunities, and institutions will be among the buyers.

MarketBeat data reveals institutional ownership at 20% and growing. The group has accumulated on balance every quarter since the IPO, ramping activity sequentially into Q1 2026, and sustaining the bullish tilt in early Q2. The Q1 earnings release provided no reasons to sell, only reasons to hold and build on positions over time.

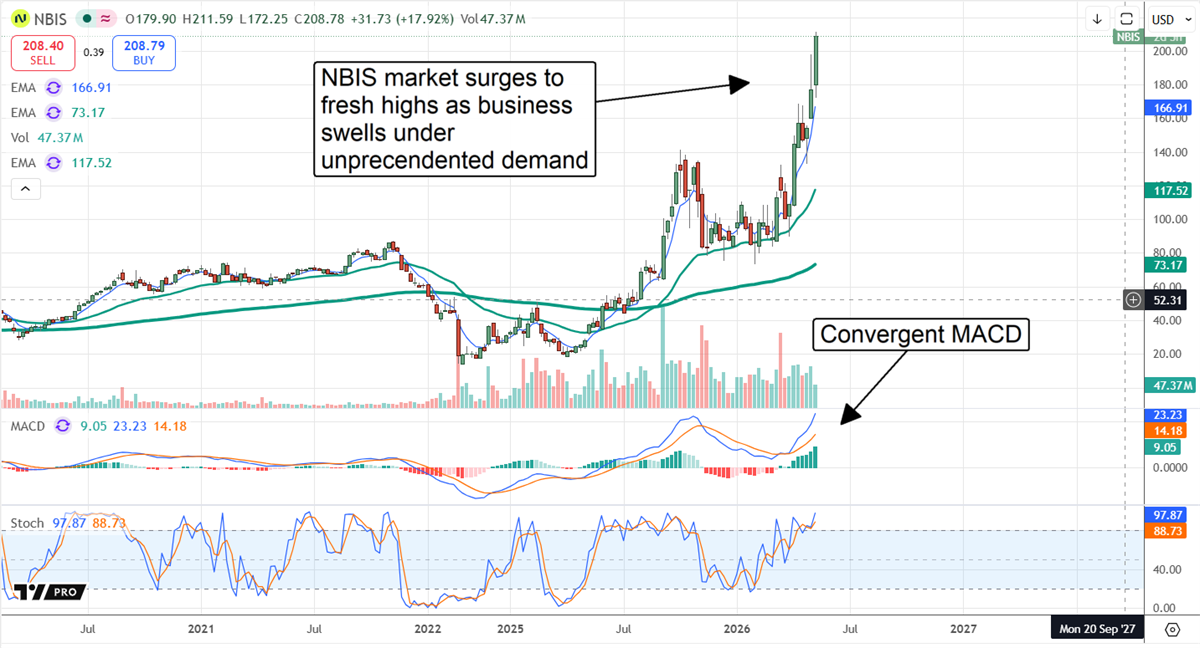

Nebius stock price action is bullish, reflecting a strengthening market with potential to continue accelerating. Signs of strength include the sequentially larger candles formed in late April and early May, as well as the convergence of MACD.

It shows market momentum is building to record highs and indicates a high probability that higher prices will be set. Technical risks include the stochastic indicator, which signals overbought conditions, but it can remain within its range for weeks and months during bull-market rallies.

Catalysts include backing from NVIDIA (NASDAQ: NVDA). NVIDIA pledged $2 billion in funding to assist the data center buildout, promising early and sufficient access to next-generation chips. The deal affirms Nebius' critical role in the AI infrastructure industry and derisks its outlook. Other catalysts include the company’s operations, which enable cost efficiency, superior performance, and reduced power consumption.

Read This Story Online |  |

| Written by Jeffrey Neal Johnson

A dramatic operational recovery is creating a powerful new narrative in the hydrogen sector. Shares of Plug Power (NASDAQ: PLUG) jumped following its first-quarter earnings report, which signaled a decisive inflection point in its path to profitability.

A 22% year-over-year revenue expansion and significantly narrower losses provided the fundamental firepower, but it was the underlying strategic execution that demanded investor attention. By aggressively expanding margins and fortifying its balance sheet, Plug Power is building a sustainable growth model. This turnaround is not only validating a bullish long-term outlook but also creating immense pressure on the over 24% of the float currently held short.

From Burning Cash to Building a Profit EngineFor quarters, Plug Power's primary headwind has been severe margin compression, but the latest earnings data shows a sharp reversal of this trend. Gross margin improved by 42 percentage points, moving from a deeply negative 55% in the prior-year quarter to a much more manageable negative 13%.

This change was not an accounting trick but the result of tangible cost-down initiatives. The Project Quantum Leap strategy, first unveiled in 2025, is now bearing fruit, evidenced by a year-over-year reduction of more than 30% in GenDrive per-unit service costs.

Simultaneously, fuel margin rates improved by 54 percentage points, driven by better leverage across the Plug Power hydrogen network and more favorable third-party sourcing contracts. This operational tightening is the core catalyst validating the bullish reversal thesis.

While the headline GAAP earnings per share figure was a loss of 18 cents, this figure includes approximately $140 million in non-cash charges, primarily related to convertible debt and warrant valuations. When these non-operational, market-driven adjustments are excluded, Plug Power's adjusted EPS stands at a loss of only 8 cents. This figure not only beat analyst expectations of a 9-cent loss but also paints a clearer picture of a business making substantial progress in its underlying economics. The performance reinforces management's guidance of achieving a positive run rate for earnings before interest, taxes, depreciation, and amortization (EBITDA) by the fourth quarter of 2026.

Funding the Future Without the Dilution DrainA key concern that has weighed on investors has been Plug Power's historic cash burn. Management is addressing this head-on with a multi-pronged strategy focused on non-dilutive capital generation, aiming to fund operations through to its positive EBITDA target without harming shareholder value. An expected $275 million is anticipated from hydrogen project asset monetizations, including a key deal with Stream Data Centers. The first transaction from this program, valued at approximately $142 million, is expected to close in June 2026.

In a more immediate cash injection, Plug Power is finalizing the sale of a Section 48 Investment Tax Credit from its St. Gabriel, Louisiana joint venture. This is projected to deliver $39.2 million in proceeds by the end of May 2026, providing a timely liquidity buffer.

Beyond asset sales, Plug Power is targeting internal efficiencies. Management has laid out a plan to reduce elevated inventory levels by at least $100 million in the second half of the year. Successfully executing this supply chain normalization represents another critical, non-dilutive source of capital to fund its growth objectives and further insulate its balance sheet.

Gridlock Is Creating a Green LightWhile near-term catalysts are focused on margins and liquidity, a powerful long-term energy narrative is solidifying the business case for hydrogen infrastructure. A growing challenge for large-scale industrial and logistics operations is the strain on local utility grids, exacerbated by the power demands of data centers and widespread electrification.

This problem has created a compelling new value proposition for Plug Power's on-site solutions. Enterprise clients such as Amazon (NASDAQ: AMZN) and Walmart (NYSE: WMT) are increasingly leveraging GenDrive and GenFuel systems as behind-the-meter power sources. This strategy allows a facility to offload roughly 2 MW of electricity demand from the grid, a significant advantage where utility power is constrained, expensive, or unreliable. This pivot from a simple productivity tool to a mission-critical energy solution represents a massive addressable market.

Disruptions in global energy markets have also renewed interest in energy security and synthetic fuels. This has been a notable tailwind for Plug Power's electrolyzer business, which saw revenues climb 343% year over year.

While international projects can face regulatory delays, Plug Power is mitigating this risk by diversifying its pipeline and advancing key North American contracts, like the 275 MW engineering design award in Quebec, which fall under a more predictable permitting framework. This domestic focus, combined with the clear demand from enterprise customers for grid independence, provides a stable, growing revenue base to complement the more complex international opportunities.

The High-Voltage Case for Plug PowerThe combination of a fundamental business turnaround and a powerful new energy narrative has created a compelling setup for Plug Power. The bull case rests on the continued recovery of margins and on Plug Power's strategic positioning as a key solution to the modern energy crisis.

As more enterprises face grid-related growth constraints, the demand for behind-the-meter solutions is poised to accelerate, providing a durable tailwind. This robust strategic positioning is what makes the large short interest a secondary, albeit potentially explosive, factor. Each milestone achieved in the turnaround plan makes a bearish thesis less tenable.

The primary risk remains execution, though Plug Power has laid out a clear, multi-faceted plan to manage its cash flow and fund its path to profitability. Should there be any stumbles in the asset monetization timeline, Plugs' aggressive inventory reduction and the imminent tax credit cash infusion provide significant operational buffers.

For investors, the focus should be on the execution of this strategy. The dramatic improvement in gross margins appears to be the definitive inflection point, suggesting that Plug Power is successfully navigating its transition from a high-growth, cash-burning innovator to a sustainable and profitable energy-tech leader.

Read This Story Online |  Louis Navellier - who manages $1.1 billion including $358 million in AI stocks - says a new AI computer being built at a classified government facility in Tennessee could make today's leading AI models obsolete overnight. He compares it to the iPhone moment that wiped out Nokia, BlackBerry, and Motorola.

When this machine comes online, it will reportedly accelerate AI breakthroughs 360-fold - compressing five years of progress into five days. Navellier has identified specific stocks he'd sell before this hits, and one ticker he'd buy before May 5th. See the full free presentation with names to buy and sell now |

| More Stories |

| |

|

|

![[Watch] FREE STOCK PICK for Elon Musk’s Starlink SuperIPO](https://www.marketbeat.com/images/webpush/files/thumb_20260204150656_pushelon-6083103640.jpg)