I've been tracking a financial revolution that most people don't even know exists yet.

It lets you generate $306 to $5,000 per month in retirement income…

With 10X less money than what financial advisors say you need!

This is a new type of investment you can buy with one click in your brokerage account.

Tim Plaehn

Lead Income Investor, Investors Alley

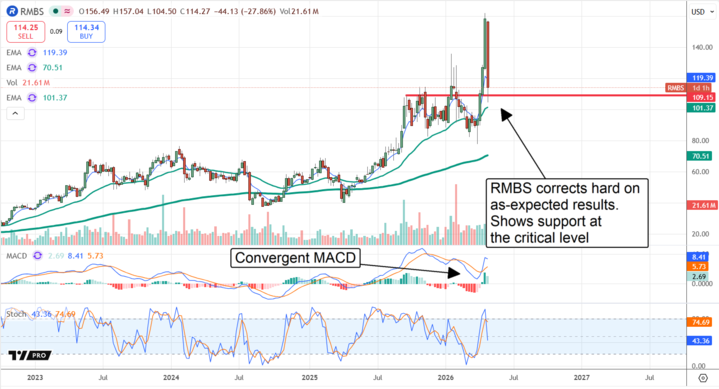

5 Reasons Rambus Stock Price Collapse Is One Hot Entry Point

Author: Thomas Hughes. Posted: 5/1/2026.

Key Points

- Rambus stock price pullback was an emotional response to less-than-expected news.

- The near-term outlook was hampered, but the long-term outlook remains robust.

- The April stock price reset was much needed, providing an opportune entry point for investors.

- Special Report: The Biggest IPO Ever: Claim Your Stake Today

Rambus’ (NASDAQ: RMBS) stock price took investors on a wild ride in April, surging to fresh highs and then collapsing after its earnings release. The late-April candlestick looks ominous — a large red candle nearly engulfing the prior two weeks — but this is one bear investors may want to embrace. While the price action raises questions, the implications are clear: Rambus is well-positioned in the AI ecosystem, has a long runway for growth, and the sell-off was — and remains — a buying opportunity.

Rambus Had a High Bar to Beat: As Expected Just Wasn’t Good Enough

Rambus' decline centered on market expectations heading into its Q1 earnings release. Expectations were very high given the strength in GPUs and datacenter demand.

The #1 stock to buy BEFORE the June S-1 filing (Ad)

When the SpaceX IPO launches, most retail investors will be locked out. The banks, funds, and insiders get in early - while everyone else waits on the sidelines.

But one small infrastructure supplier - a critical piece Musk can't scale the Colossus network without - is still trading well under institutional radar. A new briefing reveals the name and ticker at no cost.

Get the SpaceX infrastructure stock name and ticker hereOnce primarily a licenser of intellectual property (IP), the company now designs and markets an expanding lineup of memory interface products. These are not just simple connections between memory chips but advanced semiconductor technologies that enable efficient operation of GPUs, clusters and data centers.

The results ultimately affirmed the company’s positioning: product revenue grew to $88 million, nearly 50% of sales, and management emphasized long-term potential. Management sees the rise of agentic workflows and inference as the key demand driver for Rambus’ products — a market larger than the infrastructure segment and still early in its evolution. The likely outcome is continued long-term growth that could accelerate alongside wider AI adoption.

Misplaced DRAM Concerns: Acceleration Coming in 2027

One catalyst for the share decline was a downgrade from Robert W. Baird, which cut the rating to Hold while leaving its price target unchanged, citing concerns about DRAM supply. Rambus pointed to DRAM shortages as a near-term headwind to growth, but this constraint is temporary.

Manufacturers such as Micron Technology (NASDAQ: MU) and other DRAM producers are actively ramping production and capacity, with meaningful improvement in DRAM availability expected by late 2027. Rambus may therefore find it difficult to accelerate growth in the very near term, but the business remains solid and the long-term outlook robust. There is upside potential for the company to surprise in upcoming quarters and to accelerate as DRAM supply improves.

Analysts, in General, Liked What They Saw in Rambus’ Earnings Report

Robert W. Baird’s downgrade wasn’t without reason, but it was an outlier.

Most analysts responded by raising or reaffirming price targets, producing an above-consensus level that even included a new high target of $172.

MarketBeat's data shows a Moderate Buy consensus among 10 analysts, implying roughly 15% upside from a key support level and an upward trend in price targets.

The consensus of updated targets — even including Baird’s reaffirmed $120 — points to a market valuation nearer $145, about $15 above the broader consensus and on track for fresh highs.

The Price Action Is Kinda Bullish, Believe It or Not

While the recent decline suggests a deeper pullback could occur, price action, key support levels and the MACD indicator point the other way. RMBS advanced sharply from its March low, accelerating over four weeks to a new high and breaking above the DotCom-era peak for the first time in more than two decades.

The stock formed three, then four white soldiers — a bullish candlestick pattern that signals strengthening momentum and potential for further gains. The pullback has found support near prior highs, a level reinforced by increased trading volume over the past year.

The MACD is the operative signal here. Its April peak converged with the recent high and represents an extreme momentum swing — the largest on record for this stock. That pattern suggests the market will at least retest the recent high and will likely set a fresh high, the key question being whether those gains are sustained and whether even higher highs follow.

Rambus Results Weren’t Bad — No Reason to Shed 25% Here

Rambus' results were solid but fell short of lofty market expectations. Revenue grew in the high single digits, earnings rose by a slightly lower amount, and cash from operations improved by roughly 15%. The net effect was higher shareholder equity and continued ability to execute its strategy: IP development and, increasingly, product sales.

Key 2026 catalysts include expansion of the product line — notably SOCAMM2 — and the transition from DDR5 Gen2 to Gen3, which should further support growth as the market evolves.

Is This Pre-IPO AI Robotics Company the Next Big Defense Play?

Author: Bridget Bennett. Posted: 4/30/2026.

Key Points

- XTEND's AI operating system enables drone and robot autonomy across five levels, reducing operator training from months to minutes and allowing remote mission control from thousands of miles away.

- The company has active partnerships with Lockheed Martin, Ondas Holdings, Unusual Machines, and Red Cat Holdings, with its software already deployed in defense, law enforcement, and disaster response scenarios across more than 32 countries.

- XTEND is pursuing a NASDAQ listing under the ticker XTND through a planned $1.5 billion merger with JFB Construction Holdings, with the deal expected to close by mid-2026.

- Special Report: The Biggest IPO Ever: Claim Your Stake Today

The drones are already in the field. They're flying into earthquake rubble, operating in contested airspace across active conflict zones, and patrolling sites where putting a human being would mean putting that person at risk. The technology behind them isn't a prototype—it's a deployed, battle-tested AI operating system. XTEND CEO Aviv Shapira calls it "AI at the speed of flight." With a planned $1.5 billion Nasdaq listing on the horizon, the market is starting to pay attention.

An Operating System, Not Just a Drone Company

The most important thing to understand about XTEND is what it actually sells. It's not primarily a drone manufacturer competing in what Shapira calls "a race to the bottom" on hardware specs. It's a software company: an AI operating system that plugs into drones and robots made by other manufacturers and makes them dramatically smarter and easier to operate.

The #1 stock to buy BEFORE the June S-1 filing (Ad)

When the SpaceX IPO launches, most retail investors will be locked out. The banks, funds, and insiders get in early - while everyone else waits on the sidelines.

But one small infrastructure supplier - a critical piece Musk can't scale the Colossus network without - is still trading well under institutional radar. A new briefing reveals the name and ticker at no cost.

Get the SpaceX infrastructure stock name and ticker hereThe origin story matters. XTEND began in competitive drone racing, where Shapira's team discovered that the hardest part of flying a drone at 100 miles per hour through an obstacle course wasn't the hardware—it was the training time. They built software that collapsed months of FPV training into about three minutes. The follow-on insight was simple: if you could make drones that easy to fly for sport, you could make them that easy to deploy in life-or-death situations.

That pivot from gaming to defense mirrors a familiar trajectory: NVIDIA (NASDAQ: NVDA) didn't set out to power large language models; it started by rendering video games. The parallel isn't lost on Shapira, and it shouldn't be lost on investors either.

5 Levels of Autonomy and a Timeline That's Moving Fast

XTEND has mapped out five levels of drone autonomy. The company says it's already operating at levels two and three at scale, with roughly 10,000 systems deployed across more than 32 countries.

Level one is traditional manual control: one operator, one drone, hands on a controller. Level two introduces AI assistance: the drone handles the how, while the operator defines the what. Level three, which XTEND calls task autonomy, removes the operator from the field entirely. A soldier or security team 2,000 miles away can tap a window on a screen and the drone will enter a building and execute a task—"scan for survivors," for example—without manual flight control.

Level four, what Shapira calls AI pilots, is where one operator directs a swarm of hundreds of drones on a complex mission with a single prompt. Level five, still two to three years out, would have AI handle mission planning and orchestration end to end.

The response to the Turkey earthquake is a clear illustration. XTEND sent indoor drones, operating without GPS or reliable communications, into collapsed buildings to search for heat signatures of survivors. The human team didn't fly the drones through rubble; they told the drones what to look for.

The Partnership Roster

XTEND's software-first model has made it a natural integration partner for hardware names investors may already follow.

Lockheed Martin (NYSE: LMT) is co-developing a unified control system with XTEND, and the collaboration has deepened significantly. In late 2025, Lockheed's Skunk Works division integrated XTEND's XOS operating system into its MDCX autonomy platform, enabling a single operator to command multiple classes of unmanned systems simultaneously in joint all-domain command-and-control scenarios. The companies also demonstrated a "marsupial" mission, where a larger "mother" drone deploys and controls a smaller drone on target.

Ondas Holdings (NASDAQ: ONDS) is another active partner, with XTEND's software running on Ondas hardware to build aerial defense systems capable of detecting and intercepting hostile UAVs—a use case that has moved from theoretical to urgent in recent conflicts.

Unusual Machines (NYSE American: UMAC), based in Orlando, supplies U.S.-made components—motors, batteries, flight controllers—that feed XTEND's production at its Tampa manufacturing facility.

Red Cat Holdings (NASDAQ: RCAT) is listed among competitive peers in the drone space, though competition and collaboration in this ecosystem often overlap. Boston Dynamics is also using XTEND's software on its platforms, extending the company's footprint into ground robotics alongside aerial systems.

Government Contracts and Proven Demand

The partnership roster is notable, but the contract wins are where investor attention should focus. In December 2024, XTEND secured an $8.8 million DoD contract through the Irregular Warfare Technical Support Directorate to deliver its Precision Strike Indoor and Outdoor drone system—the first DoD-approved indoor/outdoor flying loitering munition platform of its kind. Then in November 2025, the company won an additional multi-million-dollar contract from the Office of the Assistant Secretary of War for Special Operations to develop and deliver next-generation AI-enabled one-way attack drone kits.

Active users of XTEND's systems now include the U.S. Department of Defense, SOCOM, the Israel Defense Forces, Singapore, and allied European defense forces. Production is scaling out of the company's Tampa headquarters, which opened in July 2025 alongside a $30 million extension to a $70 million Series B round.

The Merger and the Path to Public Markets

XTEND is currently private, but a merger with JFB Construction Holdings (NASDAQ: JFB) is in process. The all-stock deal is valued at $1.5 billion, with the combined company to be renamed XTEND AI Robotics and expected to trade on Nasdaq under the ticker XTND. The transaction is expected to close by mid-2026, pending regulatory approvals and S-4 effectiveness.

Under the deal's terms, current XTEND shareholders would own approximately 70% of the combined company, with JFB shareholders retaining roughly 30%. The merger has been approved unanimously by both boards.

What to Watch

The S-4 filing will be the first public look at XTEND's financials and business structure—a significant data point for anyone tracking this space. The company reports a $500 million pipeline, $71 million in backlog, $152 million in investor commitments, and $42 million funded to date.

The upside case is that an AI operating system designed for drones and robots sits in a structurally different position than the hardware makers it partners with. If autonomy scales the way Shapira describes, the software layer may be the most defensible part of the stack. The risks are execution-related: international expansion, closing and integrating a pending merger, fulfilling active government contracts, and competing against well-funded rivals—all at once.

Keep an eye on that S-4. That's where the real picture of this company starts to come into view.

This email communication is a sponsored email for Investors Alley, a third-party advertiser of Earnings360 and MarketBeat.

If you have questions about your account, please feel free to contact our U.S. based support team at [email protected].

If you no longer wish to receive email from Earnings360, you can unsubscribe.

© 2006-2026 MarketBeat Media, LLC. All rights protected.

345 N Reid Place #620, Sioux Falls, South Dakota 57103-7078. USA..