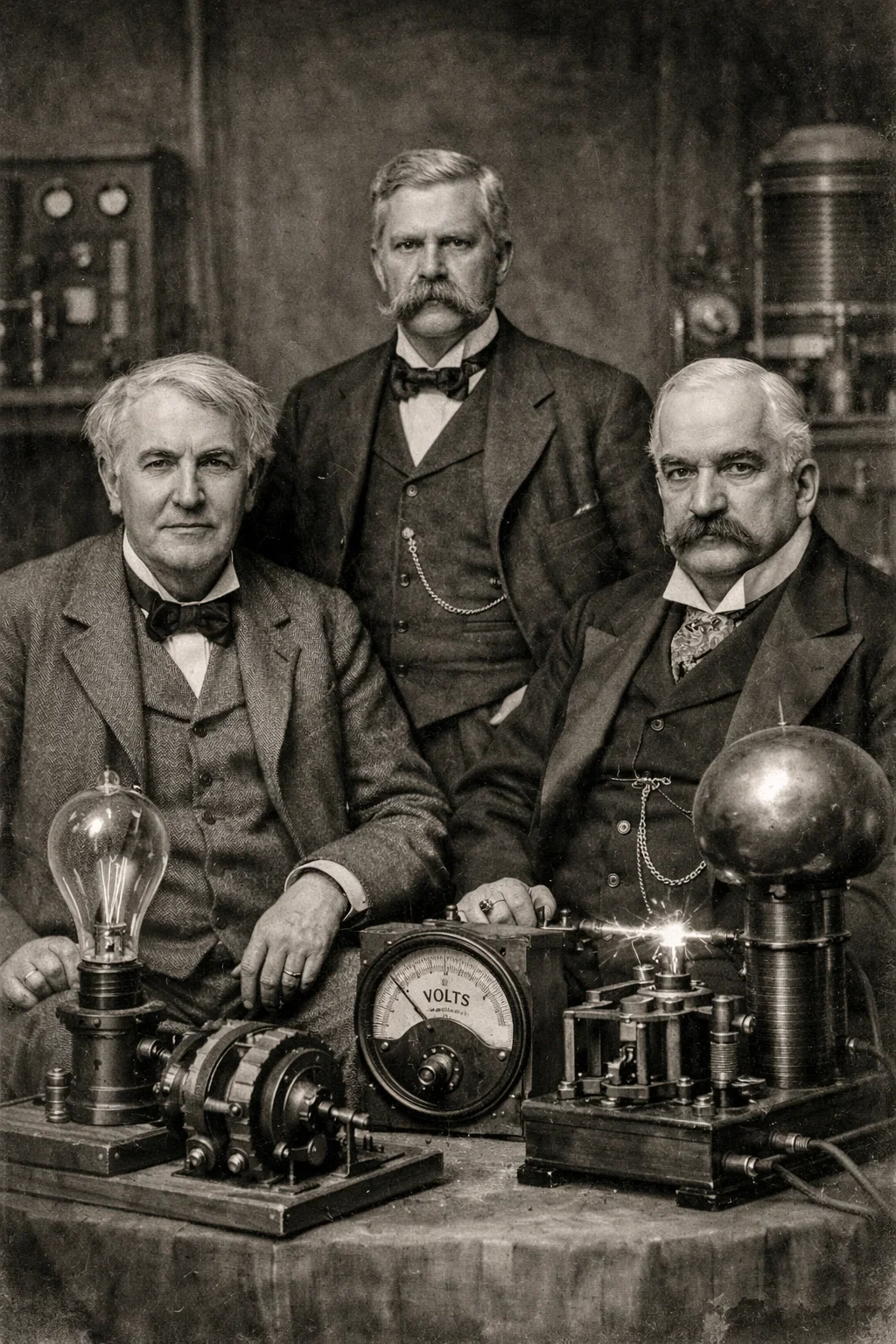

In the late 1800s, three men decided to wire America.

Thomas Edison, George Westinghouse, JP Morgan.

For decades, these men poured everything they had into copper and steel and power lines… stretching across an entire nation.

Most Americans had no idea what it meant while it was happening… the average American viewed electricity with a complex mix of awe, fear, and deep suspicion.

Viewing it as a “spooky” supernatural force instead of a modern convenience.

But the men who understood it… and positioned themselves correctly… built some of the greatest fortunes in history.

They didn’t just change the country, they changed what was possible.

The same thing is happening today…

Jeff Bezos, Mark Zuckerberg, Sundar Pichai, Satya Nadella.

They’ve decided to wire America again.

Not with copper and power lines.

With the digital infrastructure of the next American economy.

And they’ve already committed $700 billion to build it… this year alone.

The last time men this powerful decided to rewire America, it minted fortunes that could be echoed for generations.

Chris Rowe has spent 30 years studying moments exactly like this one, the moments most Americans miss while they’re busy watching the news.

He believes he knows what it means for everyday investors right now.

And he’s put together a free presentation that explains exactly where the opportunity is hiding.

To your wealth,

Bill Spencer

Cathie Wood Is Buying Tesla—Should You?

By Sam Quirke. Posted: 4/15/2026.

Key Points

- Cathie Wood’s funds have been recently buying Tesla, even as the stock’s downtrend sinks to fresh lows.

- However, bullish catalysts like FSD approval and promising analyst updates are starting to align, even as delivery data disappoints.

- With earnings due next week, Tesla is shaping into a high-risk, high-reward setup where anything could happen.

- Special Report: Elon Musk’s $1 Quadrillion AI IPO

Shares of Tesla Inc (NASDAQ: TSLA) began April in a clear downtrend, well off their December all-time high. While the stock hasn't recorded a fresh low in nearly a week, the broader picture still points to weakening momentum and fading confidence.

Which is what makes investor Cathie Wood’s recent move notable. Over the past week, her ARK funds added roughly $28 million of Tesla stock, stepping in while sentiment remains fragile and the company's narrative is under scrutiny.

ALERT: Drop these 5 stocks before the market opens tomorrow! (Ad)

The Wall Street Journal is already raising the alarm about a potential market crash, and Weiss Ratings research points to the first half of 2026 as a particularly rough stretch for certain holdings.

Some of America's most popular stocks could take serious damage as a radical market shift plays out. Analysts at Weiss Ratings have identified five names you may want to remove from your portfolio before this unfolds.

If any of these are in your portfolio, now is the time to review your positions.

See the 5 stocks to avoidWith earnings due next week, investors are left to wonder whether this is a savvy buy at a potential inflection point or another high-risk wager in a stock that still has a lot to prove. There are arguments on both sides—here’s a look at each.

Cathie Is Back: Tesla's Long-Term Potential

Since Tesla reframed itself from a carmaker to a tech-forward company, Wood has leaned into that pivot. She treats Tesla less like a traditional automaker and more like a long-term leader in autonomy, artificial intelligence, and robotics.

Near-term setbacks such as disappointing delivery figures or margin pressure are viewed as secondary to the company's potential. What matters to long-term bulls is progress toward that broader vision, and there have been encouraging signs recently.

Most notably, Tesla secured its first European approval for supervised Full Self-Driving, a milestone that lends real-world validation to its autonomy ambitions. While still early, regulatory progress like this is exactly what long-term supporters have been waiting for.

For Wood, developments like these likely reinforce the view that the recent pullback is an opportunity rather than a warning sign.

The Bear Case Has Not Gone Away

That said, the reasons behind the recent weakness are still very real. Tesla’s latest delivery report disappointed, raising concerns about slowing demand, rising competition, and the need for ongoing pricing adjustments. An inventory build has also added to the worry.

These are significant issues for a stock that still trades at a premium. Even amid a prolonged downtrend, Tesla’s price-to-earnings ratio remains in the triple digits, indicating the market is pricing in substantial future growth.

That division is reflected in analyst opinions. Firms such as RBC, Deutsche Bank, and Robert Baird have reiterated Buy or equivalent ratings this month, with price targets as high as $538 — implying nearly 50% upside. By contrast, last month BNP Paribas set a $280 target and an Underperform rating. Tesla has always attracted polarized views, and that split highlights the tension between stabilizing the core business and pursuing an ambitious long-term strategy.

Price Action Suggests a Turning Point Could Be Near

From a price-action perspective, the setup has begun to favor the bulls. The fact that Tesla hasn’t made a new low since last week suggests selling pressure may be easing.

After such a relentless selloff, sentiment appears close to being washed out. That creates an environment where even a modest positive surprise in next week’s earnings could trigger a sharp upside move — and Tesla has a history of producing precisely those kinds of rebounds.

This is likely what investors like Cathie Wood are positioning for. The structural risks remain, but the potential reward is looking increasingly compelling to some.

Earnings Will Decide a Lot

All of this sets up a critical moment for Tesla, which is due to report Wednesday, April 22. With the stock down considerably and sentiment weak, the bar for positive market reaction is lower. If Tesla shows stable vehicle demand and continued traction in areas like autonomy, momentum could shift quickly.

For more cautious investors, however, the same event presents downside risk. If the report reinforces worries about slowing growth or persistent margin pressure, the downtrend could resume.

That is what makes the current setup so interesting: Cathie Wood is effectively leaning into uncertainty, buying ahead of a major catalyst in the belief that Tesla’s long-term story will outweigh near-term noise. Whether that proves to be the right move remains to be seen.

Microsoft’s Copilot Problem Isn’t What You Think

By Chris Markoch. Posted: 4/12/2026.

Key Points

- Microsoft’s Copilot adoption is meaningful but still small relative to its overall business.

- Investor expectations for AI monetization may be outpacing reality.

- The stock’s pullback has created a valuation closer to the broader market.

- Special Report: Elon Musk’s $1 Quadrillion AI IPO

Microsoft Corp. (NASDAQ: MSFT) continues to trade near its 52-week low and is one of the worst-performing "Magnificent Seven" stocks — a group that's been much less magnificent in 2026. One reason for the sour sentiment is Copilot, the company’s artificial intelligence (AI) tool that integrates with its Microsoft 365 productivity suite.

In Microsoft’s Q2 2026 fiscal-year earnings report, it reported 15 million paid Microsoft 365 Copilot seats — the first time the company disclosed a paid-seat figure for Copilot — which left analysts and investors wanting more.

At $30 per user per month, 15 million seats are meaningful. But they’re small compared with the revenue Microsoft generates from products like Azure and its huge installed user base.

ALERT: Drop these 5 stocks before the market opens tomorrow! (Ad)

The Wall Street Journal is already raising the alarm about a potential market crash, and Weiss Ratings research points to the first half of 2026 as a particularly rough stretch for certain holdings.

Some of America's most popular stocks could take serious damage as a radical market shift plays out. Analysts at Weiss Ratings have identified five names you may want to remove from your portfolio before this unfolds.

If any of these are in your portfolio, now is the time to review your positions.

See the 5 stocks to avoidHere the debate around Copilot can feel detached from the overall business. It’s like a food critic going into a pizza parlor and critiquing the hamburger. Copilot is being treated as if it's the primary revenue driver of the company, when a more accurate view is that it's a premium, nice-to-have add-on to an already dominant platform.

Expectations Versus Adoption

The issue with Copilot largely comes down to framing. Some investors have treated Copilot adoption as a referendum on Microsoft’s entire AI future, but that’s a bigger leap than the business itself has justified so far.

Microsoft remains a platform company with a deep enterprise moat, massive recurring revenue, and an enviable distribution advantage. Copilot may ultimately become an important monetization layer, but it does not need to become the dominant revenue driver for the investment case to remain intact.

That is why the debate can feel disconnected from the business. Investors are looking for Copilot to deliver a fast, visible payoff, while Microsoft’s model typically unfolds on a slower timeline.

Microsoft has built its lead by turning distribution into durability, and Copilot follows that pattern. It’s being embedded into products customers already use, so the upside may show up in retention, pricing power, and broader usage across Microsoft’s ecosystem rather than a dramatic standalone revenue figure.

That matters because AI does not have to produce an instant spike to be valuable. In Microsoft’s case, the more important question is whether Copilot makes Microsoft 365 stickier, deepens enterprise relationships, and strengthens the case for larger cloud commitments.

Those effects may be incremental in the short term, but they can compound over time. The market often seeks a clean narrative and a single headline number. Microsoft is offering something subtler: a feature that can improve the economics of an already elite business.

Is Copilot Worth a 36% Drop in Market Cap?

Since the sell-off in MSFT began in October 2025, the company’s market cap has fallen by roughly 36%. Not all of that decline is due to Copilot metrics. Investors are also concerned about the capital expenditures (CapEx) required to expand the company’s data-center footprint.

Some even question whether all that capacity is necessary. More importantly, investors want clarity on when they’ll see meaningful returns from those billions in spending.

Following the earnings report — which reiterated its CapEx plans — Copilot has become the focal point for many investors, perhaps to their own detriment.

Microsoft may not need Copilot to become a blockbuster for the stock to work, but investors keep holding it to that standard. The company remains a fundamentally strong platform business — Copilot is only one part of the story.

MSFT Stock Offers Real Value

In early April, MSFT is trading at roughly 28x forward earnings. That’s only a touch above the S&P 500's average price-to-earnings — far below the premium normally afforded to technology names like Microsoft.

That’s why analysts’ expectations matter, and they paint a fairly bullish picture. The consensus price target of $588.97 is nearly 60% above the stock’s price at the time of writing. A handful of low estimates pull the average down, but 40 of 45 analysts rate MSFT a Buy.

What may be missing is buying volume to give the stock momentum, which likely won't arrive until Microsoft reports earnings in late April. If geopolitics calm and investors refocus on fundamentals, MSFT should attract growth-hungry buyers looking for companies with meaningful upside potential.

This email content is a sponsored email provided by True Market Insiders, a third-party advertiser of MarketBeat. Why did I receive this email content?.

If you need assistance with your newsletter, please feel free to contact MarketBeat's South Dakota based support team at [email protected].

If you would no longer like to receive promotional emails from MarketBeat advertisers, you can unsubscribe or manage your mailing preferences here.

© 2006-2026 MarketBeat Media, LLC. All rights reserved.

345 N Reid Pl. #620, Sioux Falls, S.D. 57103. United States of America..