Email

Use the 2026 Tax Brackets Like a Pro – How Retirees Can Shrink Lifetime Taxes

| From | American Retirement Insider <[email protected]> |

| Subject | Use the 2026 Tax Brackets Like a Pro – How Retirees Can Shrink Lifetime Taxes |

| Date | January 11, 2026 7:03 PM |

Links have been removed from this email. Learn more in the FAQ.

Links have been removed from this email. Learn more in the FAQ.

Most retirees focus on minimizing taxes this year.

The real opportunity lies in minimizing taxes over a lifetime.

With the IRS now publishing the 2026 tax brackets and thresholds, retirees have a rare planning window — one that allows you to deliberately move money at lower tax rates before Required Minimum Distributions (RMDs), Social Security taxation, and higher income years collide.

This is where strategic Roth conversions come in.

[link removed]

Sponsored Content

Tiger Woods Leaves the Audience Shocked Live Today

[link removed]

[link removed]

When the cameras were rolling, he dropped something that had everyone gasping. This isn’t just news—it’s a moment the sports world won’t forget.

See What Happened

[link removed]

[link removed]

[link removed]

[link removed]

[link removed]

[link removed]

[link removed]

[link removed]

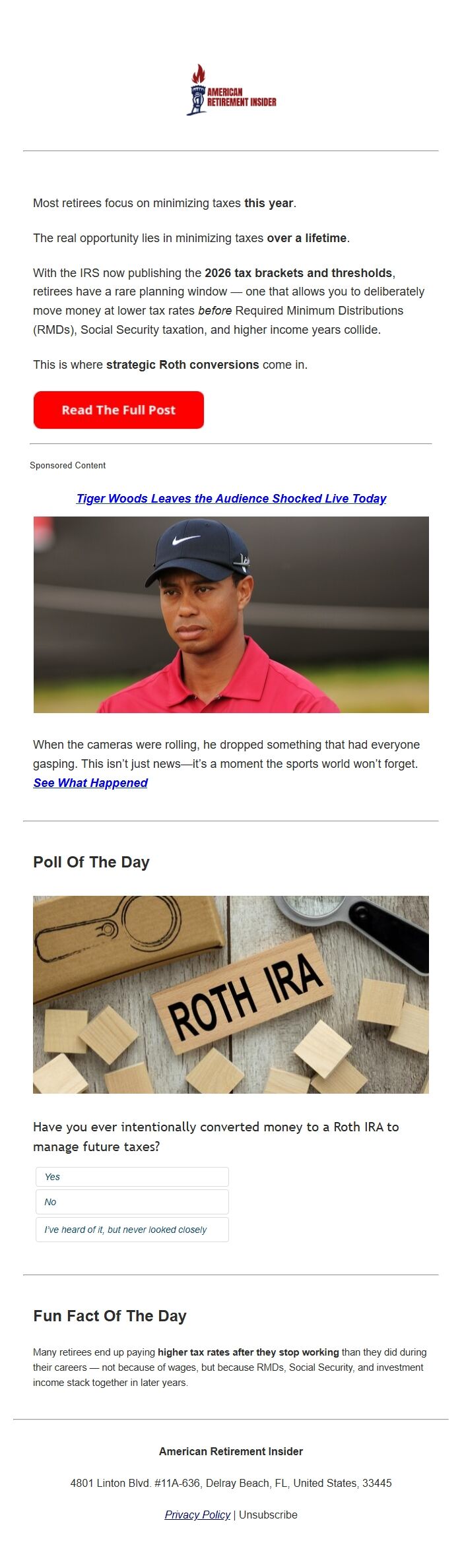

Poll Of The Day

Have you ever intentionally converted money to a Roth IRA to manage future taxes?

Yes

[link removed]

No

[link removed]

I’ve heard of it, but never looked closely

[link removed]

Fun Fact Of The Day

Many retirees end up paying higher tax rates after they stop working than they did during their careers — not because of wages, but because RMDs, Social Security, and investment income stack together in later years.

American Retirement Insider

4801 Linton Blvd. #11A-636, Delray Beach, FL, United States, 33445

Privacy Policy

[link removed]

|

Unsubscribe

[link removed]

The real opportunity lies in minimizing taxes over a lifetime.

With the IRS now publishing the 2026 tax brackets and thresholds, retirees have a rare planning window — one that allows you to deliberately move money at lower tax rates before Required Minimum Distributions (RMDs), Social Security taxation, and higher income years collide.

This is where strategic Roth conversions come in.

[link removed]

Sponsored Content

Tiger Woods Leaves the Audience Shocked Live Today

[link removed]

[link removed]

When the cameras were rolling, he dropped something that had everyone gasping. This isn’t just news—it’s a moment the sports world won’t forget.

See What Happened

[link removed]

[link removed]

[link removed]

[link removed]

[link removed]

[link removed]

[link removed]

[link removed]

Poll Of The Day

Have you ever intentionally converted money to a Roth IRA to manage future taxes?

Yes

[link removed]

No

[link removed]

I’ve heard of it, but never looked closely

[link removed]

Fun Fact Of The Day

Many retirees end up paying higher tax rates after they stop working than they did during their careers — not because of wages, but because RMDs, Social Security, and investment income stack together in later years.

American Retirement Insider

4801 Linton Blvd. #11A-636, Delray Beach, FL, United States, 33445

Privacy Policy

[link removed]

|

Unsubscribe

[link removed]

Message Analysis

- Sender: n/a

- Political Party: n/a

- Country: n/a

- State/Locality: n/a

- Office: n/a