|

|

Thank you for being a free subscriber.. Don’t lose access to Lincoln Square. If you upgrade right now, you can lock in 30% off forever. This offer ends on Oct. 31st.

Join us on the frontline in the battle for our rights and freedoms under the law. It's our duty as Americans to defend democracy. Together. Your subscription upgrade helps us inform disengaged voters with the facts to mobilize them into action!

Confused about Health Plans after Trump's Cuts? We've Got You Covered.

Your guide to the ACA Open Enrollment Period for 2026 is here.

|

Almost exactly a year ago, I began my 2025 ACA Open Enrollment Period guide with the following words:

This is the best OEP ever for the ACA for several reasons:

The expanded/enhanced premium subsidies first introduced in 2021 via the American Rescue Plan, which make premiums more affordable for those who already qualified while expanding eligibility to millions who weren’t previously eligible, are continuing through the end of 2025 via the Inflation Reduction Act;

A dozen states are either launching, continuing or expanding their own state-based subsidy programs to make ACA plans even more affordable for their enrollees;

100,000 or more DACA recipients are finally eligible to enroll in ACA exchange plans & receive financial assistance!

What a difference a year can make.

The first and third bullets above are, sadly, no longer the case: Not only are DACA recipients no longer eligible to enroll in ACA coverage, neither are several other classes of non-citizens, including those who were granted asylum for fear of being tortured and even victims of domestic abuse and human trafficking.

In addition, of course, the enhanced federal tax credits which have been a godsend over the past 5 years are still scheduled to expire just over two months from today, largely causing gross premiums to jump by 25% on average and NET premiums to skyrocket by 114% on average nationally starting January 1, 2026.

So no, I’m not gonna put on a cheery face: If the 2025 Open Enrollment Period was the best ever for the ACA, the 2026 OEP is gonna be the worst ever for most of the ~22.7 million current enrollees as well as the millions of others who might be considering newly enrolling in ACA coverage.

Welcome to TrumpCare 2.0.

Having said that, there are still some bright spots (or at least less dim ones). For starters, the second bullet above is still mostly accurate: There are ten states (down from twelve) newly-offering or retooling state-based subsidy programs to cancel out some of the lost federal tax credits or which are newly-implementing other policies to help mitigate the damage.

Beyond that, most of the other enrollment tips I give every year remain good advice, even if they kind of feel like slapping a Band-Aid® on a gaping gunshot wound this year.

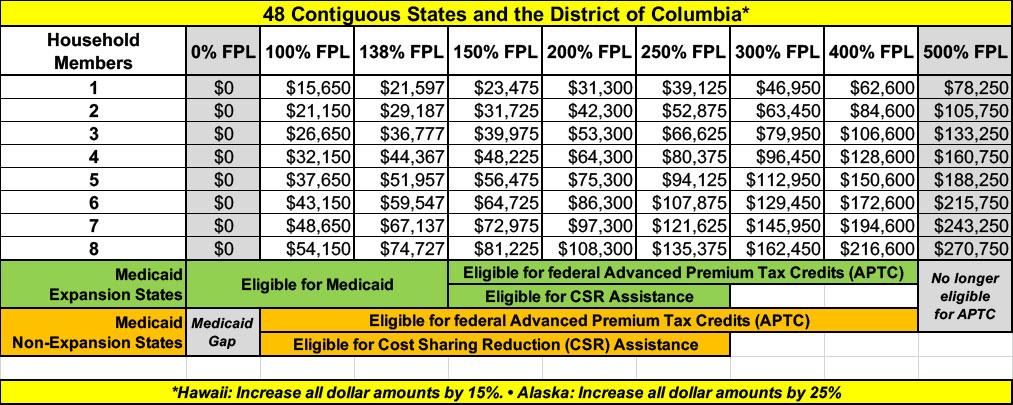

NOTE: Before I begin, it’s important to know what the Federal Poverty Level (FPL) will be in 2026. The FPL is a critical part of the formula used to determine eligibility for both premium tax credits as well as Cost Sharing Reduction (CSR) subsidies and Medicaid expansion eligibility in the states which have expanded the program. In addition, the FPL threshold goes up by a few percent each year due to inflation.

This table breaks out the key annual income levels for different FPL thresholds based on the number of members in the household. Note that all of these levels are 15% higher in Hawaii and 25% higher in Alaska:

|

With all of that in mind, here are some important things to know when you #GetCovered.

1. DON’T DELAY; GET COVERED SOONER RATHER THAN LATER!

The 2026 Open Enrollment Period officially runs from November 1st, 2025 through January 15th, 2026 in most states, but there are some exceptions at both ends:

Idaho already launched their 2026 OEP on October 15th, and it only runs through December 15th.

Massachusetts’ OEP ends, as usual, on January 23rd, 2026.

Virginia‘s OEP ends on January 30th, 2026.

California, DC, New Jersey, New York and Rhode Island have final deadlines of January 31st, 2026.

In most states you have to enroll by December 15th in order for your coverage to start on January 1st, with a few exceptions. Otherwise it won’t start until February 1st, 2026. Again, there’s a few exceptions:

Idaho: The December 15th deadline is the only one (no February eligibility)

Massachusetts: December 23rd for January 1st coverage

Maryland, Nevada, New Jersey, New Mexico and Rhode Island: December 31st for January 1st coverage

There are some exceptions to the above:

Members of federally-recognized Native American tribes or Alaska Natives can enroll in ACA coverage year round.

There are several state-specific programs which allow eligible enrollees to do so year round, including:

Connecticut: Covered Connecticut

District of Columbia: Healthy DC (Basic Health Plan)

Massachusetts: ConnectorCare

Minnesota: MinnesotaCare (Basic Health Plan)

New York: Essential Plan (Basic Health Plan)

Oregon: Bridge Program (Basic Health Plan)

I’ll discuss each of these in more detail below.

In addition, people who are eligible for Medicaid or the Children’s Health Insurance Program (CHIP) are eligible to enroll in those programs year-round.

IMPORTANT: Residents who earn less than 150% of the Federal Poverty Level (FPL) used to be able to enroll year-round, but the Trump Regime has ended this.

If you want to enroll outside of the dates above and aren’t eligible for any of the exceptions listed, you’ll likely have to qualify for a Special Enrollment Period (SEP).

Qualifying Life Experiences (QLEs) which make you eligible for a SEP include things like:

Losing employer-sponsored healthcare coverage

Getting married or divorced

Giving birth/adopting a child

Turning 26 and having to move to your own policy

Losing eligibility for Medicaid or CHIP

Moving out of your current rating area

2. ONLY ENROLL VIA AN OFFICIAL ACA HEALTH EXCHANGE OR AN AUTHORIZED ENROLLMENT PARTNER.

ACA financial subsidies are only availalble to eligible enrollees who sign up through an official ACA exchange or an authorized 3rd-party exchange entity, known as an Enhanced Direct Enrollment (EDE) entity.

There’s a ton of junk plans and scam artists out there, especially these days. Fraudulent plans are being hawked endlessly via both robocalls, spam emails and fly-by-night websites.

IMPORTANT: Scams & Junk Plan pitches are going to be an even worse problem for 2026 because of the expiring tax credits & other Trump regime policy changes which are making it more difficult for people to enroll in legitimate ACA plans or to qualify for legitimate financial help.

If you’re enrolling online, make sure to use one of the official ACA exchange websites:

As for EDEs, it’s important to note that some of these may also sell non-ACA compliant plans. The largest EDE, HealthSherpa, only sells on-exchange ACA-compliant policies. Full disclosure: They advertise on this website.

Also note that while some insurance carrier websites are also hooked into the federal exchange via an EDE, they (understandably) only list their own plans. I still recommend only using one of the websites listed above. Remember, whether via an official exchange site or an EDE, you have to enroll on-exchange to be eligible for financial help!

On a related note ...

3. IF YOU’RE ENROLLED OFF-EXCHANGE, SEE IF YOU CAN ENROLL ON-EXCHANGE INSTEAD.

As far as I can figure, somewhere around ~2 million Americans are still enrolled in OFF-exchange, ACA-compliant individual market policies. Historically, the main reason for this has been that they didn’t qualify for financial help, so didn’t see the point of filling out any additional forms by enrolling on-exchange.

The reality, however, is that many of these off-exchange enrollees may have been eligible for ACA subsidies after all if they had enrolled in the exact same plan but had done so via their ACA exchange instead of directly through the carrier.

With the enhanced tax credits expiring, there’s going to be a lot fewer people who benefit by moving from off-exchange to on-exchange plans, but I’d still strongly urge people to at least check into it, especially if there’s any chance of your 2026 household income being being less than 400% FPL (see the table above for how much that will be).

Full-price/unsubsidized ACA premiums are increasing by a whopping 25% on average next year, so I can’t stress this enough: If you enroll off-exchange, there’s a chance you’ll be leaving thousands of dollars in savings on the table.

Charles Gaba is a health care analyst who tracks policy and politics at ACASignups.net. He also runs Blue26.org, which makes it easy to donate to Democratic candidates at the federal, statewide, and local levels.

There’s a lot more to this guide! Read more from Charles here.

A guest post by

|

You’re currently a free subscriber to Lincoln Square Media. For full access to our content, our Lincoln Loyal community, and to help us amplify the facts about the assault on our rights and freedoms, please consider upgrading your subscription today with this limited-time offer that ends Oct. 31. Get all-access and save 30% off forever. Lock in this special rate today.

Not ready to subscribe? Make a one-time donation of $10 or more to support our work amplifying the facts on social media, targeted to voters in red states and districts that we can help flip. Every $10 reaches 1000 Americans. The Truth needs a voice. Your donation will help us amplify it.

Want to help amplify this post? Please leave a comment and tell us what you think.

![]()

![]()