|

|

|

|

|

|

|

Money Metals News Alert

|

April 28, 2025

– Silver prices rallied last week, while gold prices lost a bit of ground in

some pretty volatile trading.

|

|

|

Safe-haven buying in the

futures market slowed dramatically from the week prior as risk assets including

U.S. stocks rallied. The S&P 500 gained 300 points – nearly 6% – on

the week.

The U.S. dollar regained a

bit of ground in foreign exchange markets.

Bond prices also rallied,

with yields on the 10-year bond falling not quite 20 basis points.

|

|

|

|

Markets may remain somewhat

schizophrenic while trade negotiations are ongoing and concerns over tariffs ebb

and flow.

April has seen the strongest demand

for retail bullion since the months leading up to last year???s election. The

volatility in other markets has stimulated buying. Higher metal prices have also

been driving some selling. This is helping to keep dealer inventories plentiful

and premiums down.

|

|

|

|

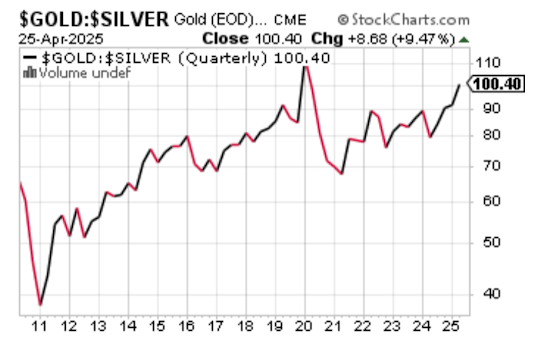

Gold : Silver Ratio (as of

Friday's closing prices) – 100.0 to

1

|

|

|

|

Gold Outperforms... Will that Continue?

|

|

|

|

|

|

There are plenty of frustrated silver

bugs. Gold is outperforming once again, and they wonder when silver will finally

catch up.

History suggests silver will outshine

gold in a bull market for metals. So far, that has not been the case for much of

gold???s current bull run which began in 2015.

It isn???t certain whether this time

will ultimately be different. Nine years into the run higher, silver remains way

below the 2011 highs. Gold broke through its prior high five years ago. Recently

the gold/silver ratio floated back above 100, an extraordinarily high figure.

(See Chart Below.)

|

|

|

|

|

Why has gold fared so much better than

silver?

The answer is complicated and some of

it is guesswork. For example, it is not possible to gauge how much influence

artificial forces such as bullion bank price rigging and algorithmic trading have

had on current metal prices. The answer, in our view, is at least some.

But given the dwindling above-ground

inventories of silver, the difficulties miners have in raising production, and the

steadily growing demand for silver, the days of lower silver prices are numbered.

|

|

|

There are other forces

which might help explain why gold has fared so well. Gold???s demand is more

concentrated. The vast majority of buying comes from investors and from central

banks. While silver has seen growing demand from investors, the metal isn???t

something central banks are stockpiling.

Industrial demand is a far

larger component in the silver market than for gold.

|

|

|

|

During periods when investors worry

about the economy, such as early months of COVID and the more recent fears over

tariffs, silver is likely to underperform. Investors anticipate less demand for

the metal from manufacturers.

While slowing demand from

manufacturers will weigh more heavily on silver prices, there is another key

difference which accrues in silver???s favor.

Silver used in manufacturing is mostly

???used up.??? It goes into products which eventually wind up in a landfill. It is

different for gold. Most of what is used in major applications like jewelry and

dentistry is ultimately recovered and recycled.

There is no largescale recycling

effort for silver. That could change as recycling processes improve, but silver

prices will likely have to be much higher before it makes sense to try to recover

silver from things like trashed electronic devices and solar panels.

|

|

|

Gold gets a lot more

demand from institutional and very large investors. The fact is it would be hard

to park $100 million on silver without impacting the price. Taking a billion

dollar position without having to pay a huge premium would be impossible.

Gold benefited during

recent weeks as huge sums of money shifted out of the equity markets, the bond

markets and even the U.S. dollar.

|

|

|

|

For a lot of money managers making

these big moves, silver isn???t even really among their options.

The safe-haven buying for silver comes

largely from retail investors, not titans on Wall Street. This buying was frenetic

from 2020 to 2023, it slowed down dramatically during 2024, and has only recently

begun picking up.

|

|

|

An environment where there

is strong demand from retail investors as well as solid industrial demand would be

ideal for silver to catch up to gold. Whether or not silver bugs will be fortunate

to get a market which fires on all cylinders is pure speculation.

The truth is the silver

market doesn???t need that much help for the metal to be repriced dramatically

higher relative to gold.

|

|

|

|

The setup in the futures market is

explosive. The recent surge in imports from vaults in London and elsewhere

provided some reprieve in the U.S., but annual deficits in new mine supply versus

demand is problematic.

Deficits will almost certainly persist

until higher prices start moving the needle on production, and this situation

keeps a floor under silver prices.

|

|

|

|

|

|

|

|

This week's Market Update was

authored by Money Metals Director Clint Siegner.

|

|

|

|

|

|

|

|

|

|

This copyrighted material may not

be republished without express permission. Offer only available through email

promotion. Offer does not apply to previous orders and may not be combined with

any other offer or program. Special shipping rates or other restrictions may apply

to international orders. The information presented here is for general educational

purposes only. Money Metals Exchange and its staff do not act as personal

investment advisors. Nor do we advocate the purchase or sale of any regulated

security listed on any exchange for any specific individual. While our track

record is excellent, investment markets have inherent risks and there can be no

assurance of future profits. You are responsible for your investment decisions,

and they should be made in consultation with your own advisors. By purchasing from

Money Metals, you understand our company is not responsible for any losses caused

by your investment decisions, nor do we have any claim to any market gains you may

enjoy. Money Metals Exchange is not a regulated trading ???exchange??? as defined by

the CFTC and the SEC.

|

|

|